German health insurance system is unique in the world

In contrast to most other countries around the world, a stand-alone private health insurance in Germany is actually a substitute for public insurance in the German healthcare system. It is an either-or choice. A decision you have to make, because health insurance is mandatory for all residents in Germany since 2009.

You can’t obtain a residence permit without proof of an existing and adequate health insurance coverage compliant to German rules and regulations. Which is why the decision to leave the public system and to join German private insurance is at least in theory a one-way-road and such a decision should not be taken lightly and without due diligence.

Private health insurance companies offer a wider coverage compared to the statutory health insurances

German private health insurance offers a wide range of different services, depending on what level the insurance plan is that you sign up for. There are basic plans that offer coverage comparable to public insurance or even lower, and there are premium plans that grant you the best possible treatment available.

Depending on your level of income and family situation, private insurance can be a very good option in terms of both cost and coverage. Privately insured people have access to doctors that don’t offer treatment to patients with public insurance, and they get appointments at many specialists often much faster. And private health insurances all offer coverage abroad, some even for periods of time longer than one year, whereas in public insurance you always need to add travel insurance in order to be covered abroad.

Advantages of private health insurance for expats

1. Get better service at family doctor, dentist and in hospital

As a privately insured patient, you generally enjoy advantages in medical treatment compared to those with statutory insurance. This is mainly due to the fact that the insurance cover includes more extensive and more modern treatment methods. For example:

Chief physician treatment in hospital

Accommodation in a single room in hospital

Reimbursement for medications

Extensive treatments at the dentist

Alternative treatment methods by naturopath

2. Avoid waiting time with specialists and hospitals

More than six out of ten Germans (62 percent) now say they have to wait too long for a doctor's appointment. This percentage has actually grown in past years, even though the German government tried to change this.

In 2012, just over one in two complained about this (52 percent); in the 2016 survey, it was already 55 percent. This is a trend that gives pause for thought. As expected, those with statutory health insurance are disproportionately affected, with 65 percent agreeing.

As you can see from these numbers, this is not a myth but reported constantly and often, so much that even the government sees this as a problem needing to be tackled (even though failing to do so). If this is not what you want, private coverage would be a sound alternative.

But why is that? It's quite simple: If you have private insurance, the doctor or dentist can charge a higher amount for the treatment or offer additional private medical services. In other words, they earn more than those with statutory insurance. That's why you get an appointment faster and are treated preferentially.

3. Have access to the most modern examination methods or treatments available

In addition, privately insured people have access to examination methods that are not offered for people with public insurance due to the higher costs or the methods being too new/modern to have made it into the benefits catalogues of public health insurances.

Doctors are very limited in terms of what they can charge public insurances, whereas they can charge a much higher cost factor to privately insured patients, which leads to a kind of two-class healthcare system in Germany (public vs. private insurance). Nevertheless, even a person with statutory insurance in Germany is well taken care of if he or she is injured or has an illness.

4. Receive a guarantee that the insurance coverage will not be reduced

The scope of benefits of the statutory health insurance is regulated in Social Code 5. The health insurance funds are obligated to provide this insurance coverage. If the legislator deletes services from the benefits catalogue, the health insurance company no longer has to cover the costs of a deleted treatment.

Private health insurance is a contract between you and the health insurance company with a precise description of the scope of benefits. The insurance coverage cannot simply be reduced by the company.

Services

German Private Health Insurance

German Public Health Insurance

Dentist

Comprehensive services

Basic services

Hospital

Chief physician, Single room

Specialist, Multi-bed room

Choice of doctor

Free choice

Only panel doctors

Specialists & physicians

Appointments possible at short notice

Often several months waiting time

Clinic selection

Free choice

Nearest clinic

Medication

Comprehensive reimbursement

Only prescription drugs with co-payment

Glasses & Vision Aids

High performance level

Only in cases of hardship

Alternative treatment methods

High performance level

Sporadic

Why expats trust us

100% English-speaking advisors - "Life is too short to learn German".

Offers from more than 150 insurance companies - with us you really have the choice

Many years of experience and specialisation - we know the needs of expats

Employees who earn above a certain threshold (in 2024 your gross income needs to be above €5,775 per month/ €69,300 per year) can opt to sign up for private health insurance instead of public insurance, employed persons whose income is lower than that are compulsory members of the statutory scheme. They should then look more at private supplementary coverage here.

Public servants (Beamte) usually will find that their only financially viable choice is to join a private health insurance plan to supplement their state health coverage.

Self-employed/Freelancers can only join the statutory scheme under certain circumstances (see chapter on public health insurance, the requirement to meet is a proven prior public insurance coverage in Germany or another EU Country for the past 12 months or at least 24 months out of the last 5 years).

Challenge for freelancers and self-employed

Freelancers and the self-employed moving to Germany who don’t qualify for public health insurance, have no choice but to go with private health insurance. Unfortunately, German private insurances are not always too keen to accept the self-employed into their ranks because they are considered to be too much of a credit-risk for the insurance in the first years. They cannot provide proven credit-history and income-info (like a tax note).

In those cases where access to a “normal” private German health insurance appears to be not possible, we at CRCIE can actually offer a unique alternative together with the ASEIG (Association of self-employed Expats in Germany) with a special group plan from a German private health insurance company open to self-employed Expats in Germany.

This is a far better alternative than using one of the many international health insurances for those living in Germany. Even though International health insurances are popular outside Germany - they usually don’t comply with the German legal requirements and regulations. Using those can lead to serious back-charges from German insurance providers later.

Costs of private health insurance in Germany

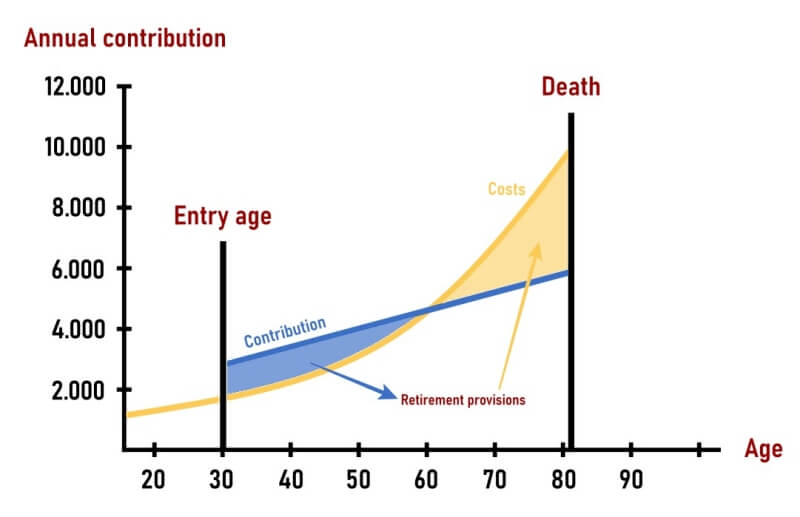

Premiums for private health insurance are not based on your income, but they are calculated by the insurer on the basis of the benefits offered, how old you are when you apply and what your health status is.

The monthly entry premiums are vastly different for the same insurance plan depending on your age at the beginning. Because German private health insurances are computed like a life insurance they’ll have to estimate the medical costs over time and split these over the estimated average life span.

Therefore, someone entering a private health insurance as a young person has much lower premiums per month over the entire duration of the health insurance than someone who starts at age 50, for example.

A myth: private health insurances become too expensive over time in comparison to public health insurance

If you look just at the development of premium increases between 2015 and 2021 you’ll see that both, public and private health insurances have increased the premium costs significantly.

According to a recent statistical survey, health insurance premiums for private health insurances increased a total of 24.7 percent from January 2015 to March 2021, while overall consumer prices rose only 9.1 percent during the same period.

This does of course look unpleasant and gives reasons to think if setting yourself up for your health care needs through joining private health insurances is such a good idea. However: for average earners in the German public health insurance, contributions increased by a total of 20.5 percent during the exact same period of time.

Thus, in 2015, the monthly contribution of an average earner in the statutory health insurance was € 457; in 2021, it is € 550. Voluntarily insured persons (those with higher incomes) in the public health insurance system with incomes in excess of the legal threshold (i.e. the highest level the public insurance premiums are computed with) paid actually € 639 per month in 2015. By 2021, their contribution has risen by 20.3 percent to € 769 a month.

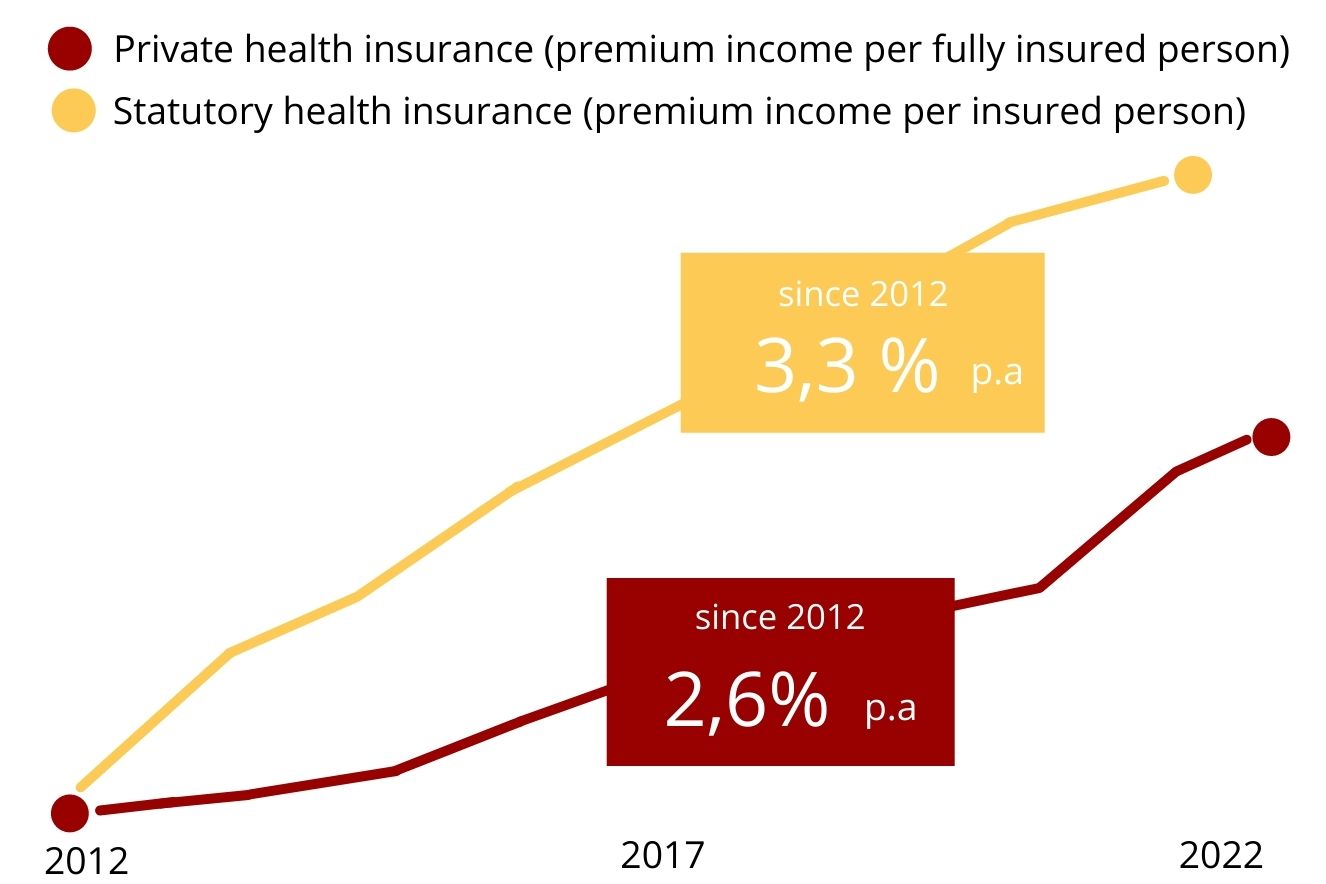

Premium development for statutory and private health insurance during the last 10 years

If we look at even more long-term developments of contributions in private and statutory health insurance we see that the two are very close to each other. Between 2012 and 2022, i.e. over the period of the last 20 years, premiums collected from insured persons in private health insurance increased by an average of 2.6 percent per year.

In the statutory health insurance, however, the figure is actually higher at 3.3 percent. This is the result of an analysis by the Wissenschaftliches Institut der PKV (WIP).

Comparison of premium development in private health insurance and statutory health insurance

If the statutory German health insurance system did not receive massive subsidies from taxes in addition to its premium income (2020: EUR 18.0 billion), these premium increases would be even higher.

Reduction of coverage: a hidden 'premium increase' in statutory health insurance

One hidden increase with public health insurance, btw., is the reduction of coverage. This can happen any time through a simple legislative act. Political and financial reasons can lead to legally guaranteed benefits being changed by the legislature. In the long term, statutory health insurance will face problems anyway.

The so-called pay-as-you-go system creates long-term financing problems for health insurance. This is because fewer and fewer young working people not only have to finance their own health care, but also have to pay the health care costs of more and more aging population. The same problem is true for the entire German social security system, including the public pension, for instance.

In the long term, this will mean higher health insurance premiums for those with statutory health insurance. On the other hand, far fewer services will probably be paid for by health insurance in the future, thus resulting in further cuts to the current coverage out of financial necessity. In theory, the resulting insurance gaps created by the law-makers within the public health insurance can be closed with the help of private supplementary health insurance.

Supplementary health insurance and its problem

The problem with supplementary health insurance is that as with private health insurance, the availability and cost of supplementary insurance depends not only on the scope of benefits selected but also on the age at which the policy is taken out, and of course also the actual state of health.

Thus, many people who are now facing serious personal co-costs for dental replacements would like to have a private supplementary coverage. However, private health insurers do not accept these people because treatment has already begun or is about to begin. And the public health insurance only pays at best 50 % of these costs, which leaves a share of costs by the patient of thousands of euros.

Had they only known in their younger years that these services of the public coverage would decrease so dramatically, they could have set up at low monthly costs a private dental insurance. But now it is just too late.

At any given time, the legislature can change or reduce the coverage. This is one of the criticisms of the system of statutory health insurance: It makes long-term financial planning for health costs so uncertain.

Inflation and medical progress: the reasons for premium increase in private health insurance

When looking at their current premiums, the vast majority of people with comprehensive private health insurance will see that their private health insurance tariffs are quite favorably priced. They offer a wide range of benefits. In a longer-term comparison over the last 20 years, statutory premiums have actually increased more than in private health insurance.

Having said that, premium increases take place almost every year. They are necessary in order to be able to finance the health care of the insured in the long term. It is not only in everyday life that everything is becoming more expensive - electricity, food, clothing, business ventures. But also, in medical care.

However, a private health insurance premium adjustment is a rigorous process that is controlled and monitored by an independent mathematical trustee. This shows that private health insurance is not a savings model compared to statutory health insurance.

However, high earners in particular usually pay less for private coverage at a young age than for voluntary statutory insurance. It is, therefore, recommended that the premium savings be invested securely to counteract rising costs in old age.

Avoid cost explosion in private health insurances

In old age, privately insured persons receive a whole range of financial relief that considerably reduces the monthly premium: For all those who joined private health insurance in 2000 or later, there is a strong "cushion" to dampen premiums in old age.

They pay a so-called statutory surcharge, the accumulated amount of which is returned to them from the age of 65 and dampens their premiums. This surcharge initially increases the respective monthly premium by 10 percent. From the age of 60, the surcharge no longer has to be paid, and the monthly premium is then automatically reduced accordingly.

Most privately insured persons who were already in private health insurance before 2000 have also added this provision to their contracts. There is nothing even remotely similar in the state health insurance system in Germany.

Statutory surcharge and elimination of unnecessary services reduces premiums in your retirement

Upon retirement, the contributions for the daily sickness allowance, which account for a larger portion of the monthly premium for many insured persons, are also eliminated. This protection against loss of earnings in the event of long illnesses at work is no longer needed in retirement, so the contribution falls accordingly.

And privately insured pensioners receive a subsidy from the statutory pension insurance for their private health insurance. The subsidy is currently 7.95 % of the payment amount of the personal pension, with the payment limited to half of the actual private health insurance contribution.

For example: Someone who has always earned the average wage over 45 years of working life currently receives about € 103 in health insurance subsidies on a pension of about € 1,300.

For civil servants, the allowance rate of their employer increases in old age, so that they have to pay correspondingly less for their supplementary private health insurance cover.

For those who fear that their retirement income will be too low to be able to afford the insurance cover undiminished, there are offers of premium relief plans to make specific additional financial provision. In many cases, employees can also take advantage of the employer's contribution for the payments to this insurance plan.

Is public health insurance cheaper during retirement?

In statutory health insurance, the contribution is based on a percentage of income. This means that it is often at first glance lower for pensioners. However, not only the statutory pension is burdened with the contribution rate to health insurance in old age.

In addition, all former employees who have voluntary statutory insurance must also pay the full contribution rate for health and long-term care insurance of around 19 % of the total capital saved on their company pension. For example, from an insured sum of € 25,000 this would end up being more than € 4,700.

Pensioners who are compulsorily insured in the public health insurance do benefit from a monthly allowance of € 164.50, but even they would still have to pay around € 1,000 in contributions for the above-mentioned sum insured.

Privately insured persons are not affected by this - they, therefore, have the corresponding sums available as a reserve for their private health insurance contributions in old age.

Voluntary public insurance clients even have to pay the percentage contribution on all their income, including capital gains, rental income or income from their spouses, up to a maximum contribution of currently around € 1,000 per month.

This primarily affects the self-employed and those who switched to the statutory health insurance late in life. Privately insured persons are again not affected by these contribution obligations and, therefore, have the corresponding sums available in turn as a reserve for their private health insurance contributions.

Important to know: It is impossible to make a blanket statement about which health insurance is cheaper or more expensive in retirement. It depends on the individual case. We can help you carefully weigh up the advantages and disadvantages of the individual models.

Selecting your private health insurance - making an educated decision

Private health insurance is a decision for life. But life circumstances can change and make it necessary to adjust the existing insurance coverage. This is also the case if the cost of a particular private health insurance has risen more rapidly than the competition in recent years so that it has become a financial burden and needs to be revisited.

Professional and independent advice is especially important for Expats, be they already long-time private insurance policyholders or now newly planning on setting up private health insurance for the future. There are a lot of myths, fake news and errors to be found on the internet about health insurances in Germany in general, and private health insurance in particular.

If you’d rather have solid facts and information that allow you to make an educated decision, professional advice by an independent broker specialized in catering to Expats is your best option.

If you are interested in signing up for private insurance, there are a number of points that you have to consider: Terms and conditions are important as you sign a contract with an insurance company, price stability differs vastly among the various insurance companies, and not every company offers the same value for your money, not to mention the scope of different entry requirements.

Especially for newly arriving Expats in Germany there are a number of private German health insurance companies that won’t accept an application in principal during the first two years of your stay in Germany.

Therefore, typical online comparisons of German health insurance plans carry little validity for Expats as they don´t include the special rules and regulations for Expats from the terms & conditions of the insurance companies. In order to be able to make such an educated decision, contact us for advice because we are the experts for Expats … especially regarding health insurances.

Change the current private health insurance

Switching from one private health insurance to another should be carefully considered. There are a number of options to contemplate if you are not satisfied with your current insurance company. However, there are also some disadvantages that need to be considered.

Rarely a good option: Cancel your private health insurance and switch to another provider

A premium increase is accompanied by a special right of termination. You can cancel your private health insurance and switch to another, cheaper provider. However, we only recommend this procedure to privately insured persons who are young and do not suffer from pre-existing conditions. This is because switching providers has considerable disadvantages:

Health check: You have to go through a health check again. Medical conditions that have developed during the time you were insured with your current plan can lead to being rejected for the optional tariff or having to pay a risk surcharge.

Loss of money: When you switch private health insurance providers, you lose a large part of your old-age capital reserves. This causes your premiums in the new insurance plan to increase more as you age in comparison to a similar older insurance plan.

Also, keep in mind that other insurers also increase their premiums at regular intervals. So, you will most likely be affected by an adjustment again in the following years.

Switching just based on an ad-hoc comparison of insurance premium costs, therefore, may not be in your best interest long-term. A professional independent advisor knows the market and can explain to you if your own insurance plan is still competitive financially or not.

Better option: Cost reduction by adjusting the insurance plan

By means of (re-)adjusting your existing insurance plan, you can lower your private health insurance premium. You have the option of excluding benefits that you do not claim. For example, accommodation in a single room during hospital stays. Or extending the waiting period for the daily sickness allowance to kick in, which can reduce your premium for the so-called “Krankentagegeld” by up to 25 percent.

Alternatively, you can consider increasing your deductible. However, it is important to consider whether the premium savings are actually worth it in relation to the possible additional costs.

Bear in mind that once benefits have been excluded, they cannot be agreed again without a new health check and waiting periods. This step must therefore be well considered and calculated beforehand.

Best option: internal change of insurance plan with the same insurance company

The highest possible premium savings of up to 45 percent can be achieved by an internal change of the insurance plan in accordance with Section 204 of the German Insurance Contract Act (VVG). In this case, you remain insured with your provider, but take out a different (more favorable/younger/newer) insurance plan with this insurance company. This procedure has several advantages:

Save money: The age reserve capital-stock you have already built up with this insurance company is retained in full.

No health check: The insurer waives a health check if the new tariff does not provide any improved benefits compared to the previous contract.

In addition, you can change your private health insurance plan internally at any time. There is no need for a prior premium increase as a trigger-event and there is a short period of time to give notice. An internal change of your health insurance plan offers a high savings potential.

Provided that a suitable alternative insurance plan can be found. Our experts will be happy to help you. We will check your options and which alternative health insurance plans are available from your provider.

last but not least

Re-entry into the statutory health insurance system

In order to escape the constant premium increases, many privately insured persons are considering a return to statutory health insurance. In doing so, they forgo the improved and guaranteed benefits that private health insurance offers in contrast to statutory health insurance.

As you could read above, over the past 20 years the yearly increases in health insurance costs of the public insurance have actually outpaced the increases in private health insurances. And the demographic challenges for the public system will continue to make the cost-side of public health insurances a heavy burden on the public social welfare system itself. Therefore, it needs to be well considered if a switch back to public health insurance is in the end really in your best interest. Provided it is possible at all.

A return into the statutory health insurance system in Germany is not easy.

For employees, this is possible if their income falls below the compulsory insurance limit, but only until the age of 55 years.

Self-employed persons must give up their self-employment and enter into an employment relationship subject to compulsory insurance in order to be able to return to statutory health insurance. Again, this is only possible under the age of 55 years.

After the age of 55, strict conditions must be met in order to return to statutory coverage as a privately insured person, which are a few and quite complicated.